I know people may find this topic to be boring and/or irrelevant, but everyone should be aware of basic tax legislature, whether you prepare your own taxes or not. Understanding the basics will help you make better decisions throughout the year that can lower your tax implication. I work hard to stick to a budget and save my money so I don’t want to give any more of my money to the IRS than I absolutely have to. I also don’t want to prepare my taxes incorrectly because tax mistakes can be really expensive to fix.

The following list includes common misconceptions about taxes that I have personally heard people mention when tax discussions have come up. Hopefully this helps people understand taxes a little better if they would like to. I am not a licensed CPA or a tax attorney so I can’t guarantee that this post is 100% accurate, and this information shouldn’t replace advice from a licensed tax professional. I merely want to give people something to think about so they educate themselves instead of giving all of their hard earned money to big government.

1. My AGI is the amount of money I make less taxes.

Your adjusted gross income (AGI) is your tax basis. You will have to pay taxes based on your AGI less your standard deduction or itemized deduction and exemptions.

Gross income includes the following:

- Wages, salaries, bonuses, commissions, and tips.

- Certain types of fringe benefits paid by your employer.

- Taxable interest (interest from savings bonds, savings accounts, etc. reported on 1099-INT).

- Qualified dividends from stocks (reported on 1099-OID).

- Taxable refunds/credits/offsets from state and local income taxes (If you itemized deductions on last year’s taxes and received a state tax refund last year you will have to report it as income).

- Capital gains (profits from the sale of property less losses).

- Alimony received (alimony must be reported as unearned income for those who receive it).

- Unemployment compensation (reported on 1099-G).

- IRA/taxable pension/taxable annuity distributions (if you are WITHDRAWING money from a taxable IRA or taxable pension/annuity).

- Rental real estate income (money you receive from renting real estate property you own).

- Income from self-employment (from a side gig, such as babysitting, or from a sole proprietorship or other business entity). YOU ARE REQUIRED TO FILE TAXES IF YOUR SELF EMPLOYMENT INCOME EXCEEDS $400/YEAR.

- Social security benefits (social security benefits may be 85% taxable based on income you receive from other sources).

- Farm income.

- Hobby income (money from selling jewelry if you make jewelry as a hobby).

- Gambling winnings less losses (i.e. if you win 500 but lose 200 you must report 300 [500 – 200]).

- Jury duty pay.

- Debt cancellation (if you settled with creditors for $5000 less than you owed, you will have to pay taxes on the 5000).

- Most court awards (court awards of punitive damages, not court awards that make you whole again).

- Some scholarships and fellowships

CHILD SUPPORT PAYMENTS ARE NOT INCLUDED IN YOUR GROSS INCOME!

Your gross income may be reduced or adjusted by the following:

- Educator expenses (up to $250 for teachers/educators).

- Certain business expenses for reservists, performing artists, and fee-basis gov’t officials.

- Health Savings Account (HAS) contributions (for those with high-deductible health plans, click here to learn more).

- Moving expenses (your move must be work related, and you must meet certain time and distance tests listed here).

- Self-employment taxes paid (self-employed individuals pay HIGHER taxes, and they are often required to pay estimated taxes semi-annually).

- Self-employed pension plan contributions or other self-employed qualified retirement plan contributions.

- Penalties paid on early withdrawal of savings (if you withdrew money from savings too early and had to pay a fee of $500 then 500 is subtracted from your AGI).

- Self-employed health insurance premiums paid (if you own your own business and don’t qualify for employer-sponsored health plan).

- IRA contributions (if you contributed to an IRA, 401k, 403b, TSP, or other employer-sponsored retirement plan and meet threshold income requirements you can deduct the amount you contributed from your AGI). You don’t qualify if you make too much money!

- Alimony paid

- Student loan interest deduction (student loan interest you paid).

- Tuition and fees paid (you may be able to reduce your AGI up to $4000, but you might benefit more from taking education credits like the American Opportunity credit or Lifelong Learning credit; you need to consult your CPA or tax preparer or run the numbers reported on your 1098-T and your REQUIRED BOOKS OR FEES through tax software).

- Domestic production activities deduction.

CHILD SUPPORT PAYMENTS CANNOT BE DEDUCTED TO LOWER YOUR AGI!

For example, let’s say you earned a salary of $42000 (reported on W2), you earned $200 in taxable interest on your savings (reported on 1099-INT), $600 mowing lawns during weekends (you were paid in checks), you contributed $3000 to your 401k, and you paid $600 in student loan interest; your AGI would be $39,200 (42000 + 200 +600 -3000 – 600).

Contributing more money to a qualified retirement plan and contributing to a Health Savings Account (HSA) if you have a high-deductible health plan can greatly reduce your gross income and tax liability. Just something to think about! : )

2. Maybe I shouldn’t ask for a raise. It will push me into the next tax bracket. I’ll end up paying more in taxes, and it will be a wash.

Taxes are more complicated than that. You only pay higher taxes on the amount of your AGI that pushes you into a higher tax bracket, and that amount is further reduced by your standard deduction or itemized deductions and your exemptions. For example, if you are single during 2014 and make over $9075 but less than 35900, you will pay $907.5 (which is 10% of 9075) plus 15% of the excess over $9075 less your standard deduction or itemized deduction if you itemize and your exemptions. You will find 2014 tax brackets and standard deduction amount here.

3. I can write off my charitable contributions, over the counter medication, and business expenses.

Here is a list of things you may be able to itemize:

- Interest you paid (home mortgage interest and points, mortgage insurance premiums, and investment interest).

- State and local income taxes or sales taxes (but not both).

- Real estate and personal property taxes.

- Gifts to charities (in most cases you must have receipts).

- Casualty or theft losses.

- Unreimbursed medical expenses (in excess of 10% of your AGI; if your AGI is $39,200 you can only deduct expenses that put your total medical/dental expenses over $3920 [39200 x .10], so if you incur $4000 in QUALIFIED medical expenses based on that income, you can only itemize $80 [4000 – 3920] and in most cases, you need receipts!) YOU CANNOT DEDUCT OVER THE COUNTER DRUGS OR STRICTLY COSMETIC SURGERY. Here is a list of allowable medical expense deductions.

- Unreimbursed employee business expenses (in excess of 2% of your AGI; if you’re a maintenance worker with an AGI of $39,200 and you spend $1000 on tools you can only deduct $216 [1000 -[39200 x .02]; Here is a list of allowable business expenses (note that you can only deduct 50% of the entertainment expense noted on the website).

- Tax preparation fees.

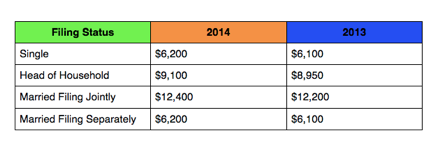

Itemization does lower your taxes by lowing your income, but it only makes sense to itemize if your itemized deductions exceed the standard deduction. The standard deduction for 2014 is as follows:

For example, let’s say you are a single maintenance man with no dependents, and you DO NOT have a mortgage. Let’s say your AGI is $39,200, based on the example in #1. You spent $1000 on work-related tools, and you tithed $500 to your local church. You also spent $1200 on medical insurance premiums, and a total of $400 on doctor/dentist copays. For Hawaii, the state income tax implication for an income or $42000 (salary to reach 39200 AGI based on the example in #1) is roughly $3818.

You can itemize your deductions for a total of $4534 as follows:

- Medical expense: 0 (you can’t deduct anything because your floor is 3920 [39200 x 10%] and you only spent 1600 [1200 health ins premiums + 400 doctor/dentist copays]).

- Business expense: $216 (1000 -[39200 x .02]).

- Charitable contributions: $500

- Hawaii state income taxes: $3818 ($42000 x 7.9%)

You will notice that $4534 is $1666 below the standard deduction of $6200. Therefore, it doesn’t make sense to itemize because you will pay more in taxes.

It’s crucial to understand how itemized deductions work so you don’t spend unnecessary or unintended money on business expenses, medical expenses, and charitable contributions.

It’s important to review last year’s AGI, mortgage interest expense statement, and state income tax statement to estimate whether or not it’s worth it to spend extra money on business/medical expenses/charitable contributions to maximize your deductions for the current tax year.

4. I shouldn’t pay off my house because if gives me a tax break.

That argument just doesn’t make mathematical sense. You can only deduct the INTEREST on your mortgage, and that’s only if it’s practical if you itemize in lieu of taking the standard deduction. I believe in home ownership, and I also believe in itemizing your mortgage when you can. Just don’t be fooled into the notion that paying off your mortgage early will cost you in taxes. It may cost you a little in pre-payment penalties, but it depends on the type of loan you have.

If you crunch the numbers I can almost guarantee that you will pay far more in mortgage interest than you will EVER save in taxes on a mortgage. Paying off a mortgage isn’t ideal for everyone. Some people need the cash flow because they are putting they’re kids through college, they lose their job, someone in the family has a chronic illness, etc. I just think it’s important to understand your options so you can do what’s best for you in your situation. I paid off my mortgage in two years, and I feel very liberated. People told me to just keep the mortgage, and I’m glad I did my research and made my own choice. I would have paid $120000 over 30 years if I had kept that mortgage. Instead I paid $68000 in two years, and now I can rent my place out and keep the extra money instead of applying it to a mortgage.

5. I don’t qualify for FAFSA. I have to get student loans.

If you or your dependents are completing their first four years of secondary education you can get a pretty substantial tax credit to help absorb the costs. If you make less than $80000, the American Opportunity credit will refund 100% of the first $2000 in qualified expenses and 25% of the next $2000 in qualified expenses for a maximum credit of $2500. The $2500 (or the amount you receive) will be subtracted from the amount of taxes you owe. The credit will be in effect through 2017.

Tuition at HCC, KCC, LCC Hawaii is typically less than $3000/year for Hawaii residents. Don’t run out and get student loans if you can help it. Student loans aren’t bankruptable, and they are a terrible burden. Avoid them if you can!

If you don’t meet qualifications for the American Opportunity Credit you may qualify for the Lifelong Learning Credit or you may be able to deduct tuition costs to lower your AGI. It’s important to explore educational tax credits when planning for college.

6. My mom/dad lives with me. I can claim them on my taxes.

Although your mom or dad may meet the criteria for a qualifying relative based on their relationship to you, there are other criteria they must meet as well.

- You must provide over 50% of their total support.

- They must have an earned income of less than $3950.

- They must not be claimed by anyone else.

Be sure to review the rules before you try to claim someone as a qualified relative.

7. I make less money so I should claim my child instead of my child’s mother/father.

This one is important in Hawaii because a lot of parents choose not to get married so they can qualify for financial aid for private school tuition.

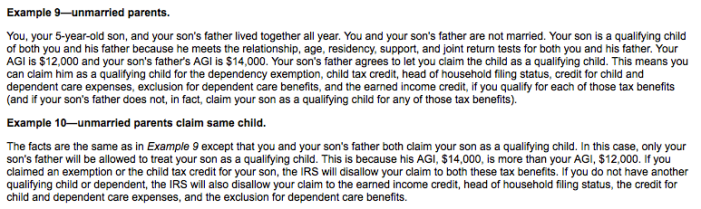

If both unmarried parents have equal custody, and both parents want to claim the child, the parent with the higher AGI should claim the child as a dependent and receive the $3900 exemption for the child. The higher earner may also qualify to file as head of household (which reduces tax liability and increases the amount of the Earned Income Credit), and he or she may qualify for the child tax credit of $1000 per child under the age of 13, the dependent care credit, and the Earned Income Credit with dependent(s). That is the rule per the IRS.

There is an exception to this example. If you live with your son and his father who has a higher AGI, you can claim your son if his father agrees to it. Here is the legislature from the IRS website.

Click here to learn more about head of household filing criteria, click here for the full list of IRS rules for claiming dependents.

8. I was unemployed most of the year. I should get a big tax refund.

Unemployment compensation doesn’t count as earned income so it won’t qualify you for the Earned Income credit, but it is reported as gross income. If you didn’t have taxes withheld from your unemployment compensation, you will have a heavy tax burden when you file. For 2013, I had to pay $2500 in taxes because I didn’t have taxes withheld from my unemployment. I really hated writing that check. Don’t be like me. If you become unemployed have taxes withheld, and don’t expect a huge refund.

But it’s something we all have to deal with. Take care! Please comment if you have any suggestions on taxes or ways to save money. : )